The devil is hiding in Footnote 2.

Last week, the crypto/legal community celebrated the OCC’s new guidance on capital treatment of tokenized securities. Basically, the bank regulator said that banks can treat tokenized securities the same as securities.

But there’s a “but”. Footnote 2 clarifies: “2 Tokenized securities that do not confer legal rights identical to those of the non-tokenized form of the security, including legal ownership rights, are outside the scope of this document. “

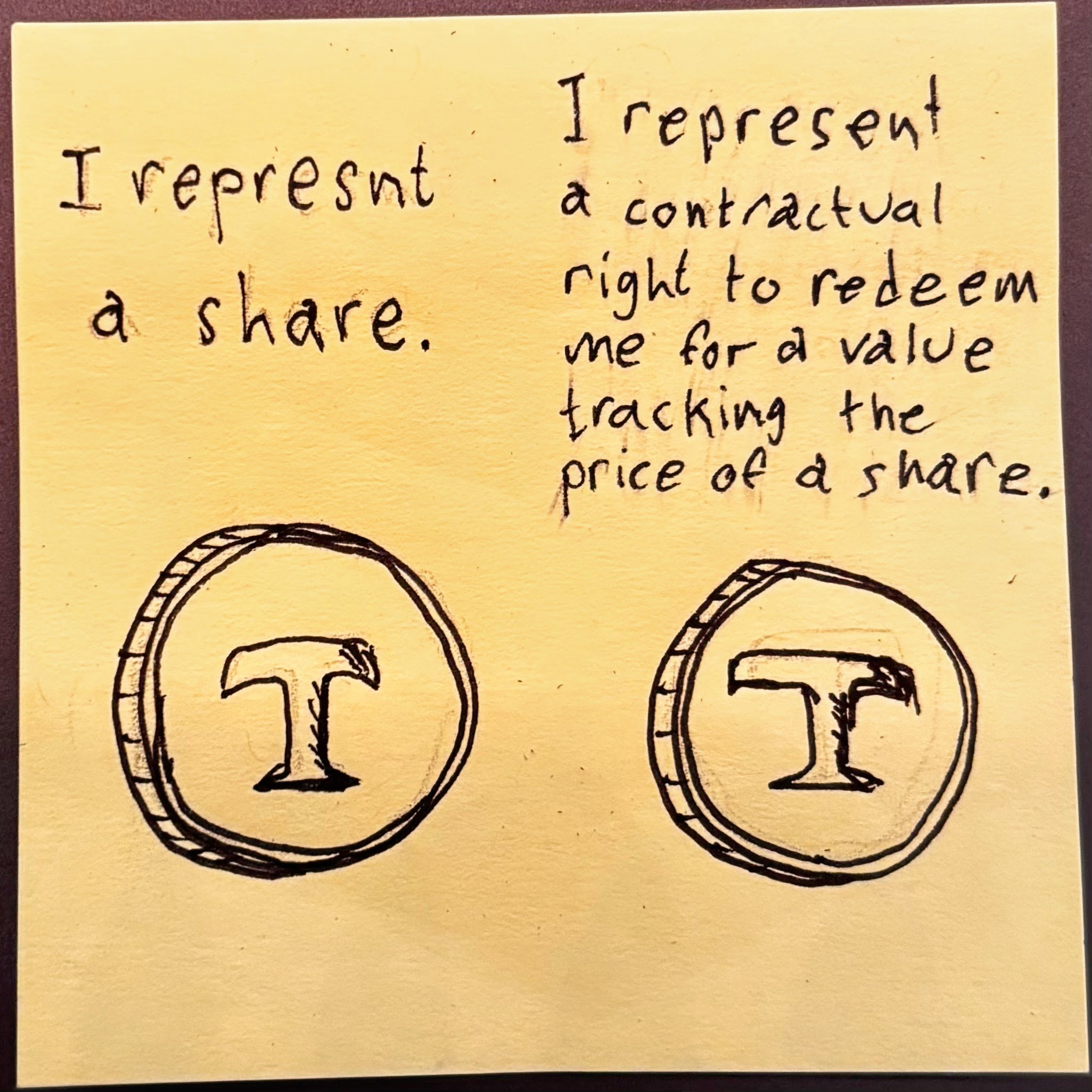

Put plainly, tokens that merely represent limited contractual claims to the value of a security but not ownership and voting rights are outside the scope of this guidance. The vast majority of tokenized public securities issued by the likes of Kraken(xStocks), Ondo Finance, and Robinhood fall into this bucket.

Today, these products are available only to non-U.S. purchasers anyway, but if they somehow end up on a U.S. bank’s balance sheet they would not count as securities. Only the tiny fraction of tokenized securities that represent full ownership rights in company stock count as securities.

Yes, the future of finance is tokenization, but not all tokenization is the same.

Not all stock tokenization is the same

The devil is hiding in Footnote 2.Last week, the crypto/legal community celebrated the OCC’s new guidance on capital treatment of tokenized securities. Basically, the bank regulator said that banks can…